BioCatch Behavioural Insights

Fraud Cases From the Wild

In our digital world, behaviour tells all.

The BioCatch Behavioural Insights Report presents an overview of fraud attack trends and insights collected by our Threat Analytics team based on their experiences working on the front lines with global customers. In these short stories, we highlight how BioCatch is delivering actionable behavioural insights to create trust and ease across the entire digital identity lifecycle.

Read the BioCatch Behavior Insights Report – June 2023 today

The Rise of Fraud and Cybercrime

Payment providers are under pressure to ensure that customer demands for convenience don’t come at the expense of higher fraud and cybercrime.

.

Payment providers have long had to balance the trade-off between meeting mandated security requirements and providing convenience and the latest technology for consumers.

Over the past five to 10 years, this pressure has become more intense, as the demand for a wider variety of fast and convenient payment options. This, however, sometimes comes at the expense of security with criminals taking advantage of the situation.

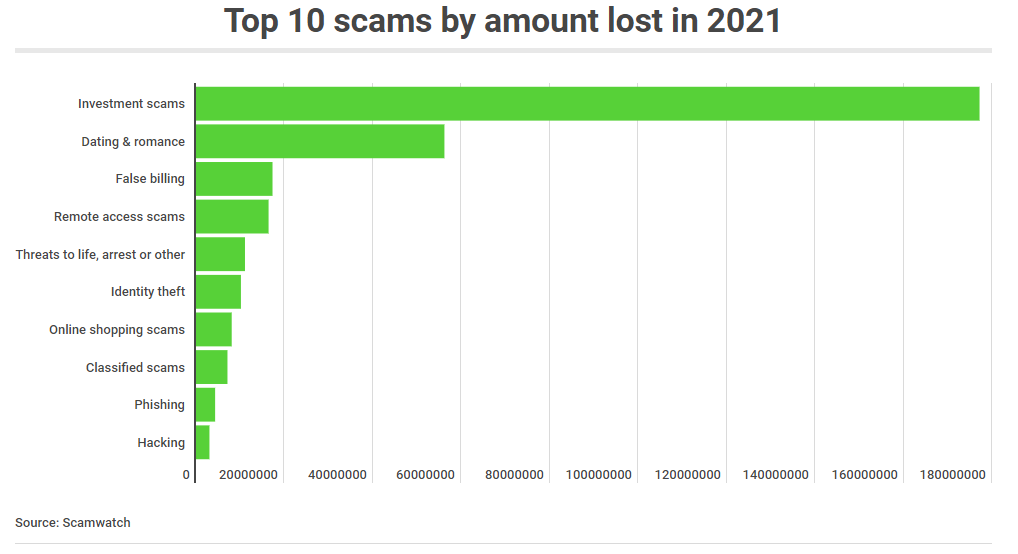

Fraud and Scams in Australia

Australians lost a record $323 million to scams in 2021. Money lost to scams almost doubled in one year, with more than 286,000 Aussies reporting they were scammed last year.

These figures represent a ‘significant’ increase of 84% compared to 2020, when Aussies lost $175.6 million through the year.

Investment scams did the most damage according to the latest figures from the Australian Competition and Consumer Commission’s (ACCC) Scamwatch.

Investment scams accounted for $177 million, followed by dating and romance scams which saw people losing $52 million.

December saw the most money lost ($43.2 million) and August 2021 saw the highest number of scams reported (40,874).

New South Wales residents were collectively duped of $110 million – the highest, followed by Victoria where residents reported $74 million lost.

Crispin Kerr, Australia-New Zealand vice president at cybersecurity company Proofpoint, said the data paints an unfortunate picture of just how effective scammers were at taking advantage of Australians in the past year.

“The 84% increase in losses to scams in 2021 is significant and is just the tip of the iceberg when it comes to understanding the true impact on Australians,” Mr Kerr said.

“Based on the numbers for December, during the holiday season, people can become desensitised to receiving numerous advertising links for shopping deals and the like and may not think twice about opening a dangerous file or clicking a suspicious link.

“The data shows scammers were extremely active in 2021 and we anticipate this will only increase as scammers continue to evolve and update their tactics.”

How are Aussies getting scammed?

While investment and romance scams were the most damaging, there were a number of other scams that saw Aussies losing millions.

Investment scams accounted for more than half of all the money lost to scams last year, and increased in prevalence by 32% compared to 2020.

“Investment scams can seem very attractive, and scammers can come across as legitimate in their promise of financial gain through the purchase of shares, funds, cryptocurrency or other high returns,” Mr Kerr said.

“However, the reality is that these get-rich-quick schemes enable scammers to steal personal and financial information to siphon funds for their own gain.”

Social media sites were the main hub for money loss via romance and dating scams, with 40% of scams reported resulting in money lost.

“Scammers also utilised social engineering particularly during lockdowns when people were at their most vulnerable to steal millions from Australians in dating and romance scams,” Mr Kerr said.

Phishing scams – where scammers aim to gain personal information – had the highest number of reports in 2021, making up one quarter of all scams reported. This is an increase of 61% on the year prior.

Scams relating to threats to life or arrest disproportionately affected younger Australians aged 18 to 24 years old, and accounted for the highest losses at $3.3 million.

Employment and job scams also more than doubled in 2021 to $2.6 million, and identity theft scams increased threefold to $10 million.

Who is getting scammed?

Older Australians suffered the greatest loss according to the ACCC’s figures, with people over 65 years old losing a total of $81.9 million throughout the year.

This demographic also reported the highest number of scams (46,282), followed by Australians aged 35 to 4 years old with 43,526 scams reported.

Men lost more to scams than women, with men reporting $190 million lost compared to $131 million reported by women.

No age group was exempt from losing money to scams, but the amount lost to scams did increase with age in 2021.

Source: https://www.savings.com.au/news/scamwatch-2021

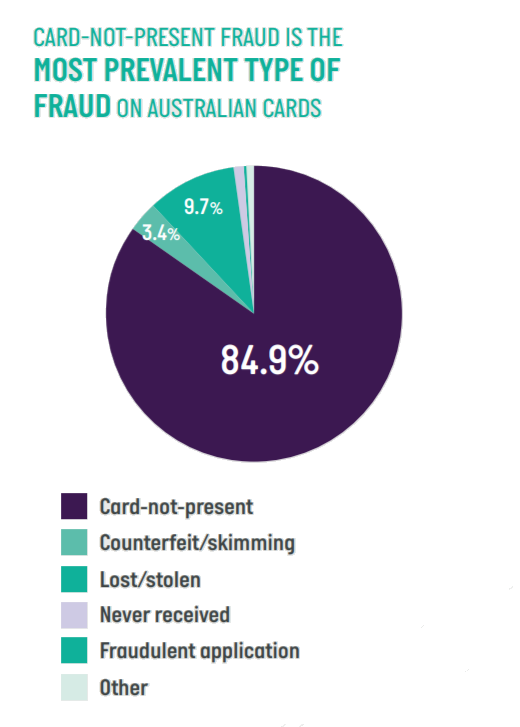

The risk of card-not-present transactions

When it comes to card fraud, however, card not present (CNP) transactions continue to dominate, making up 87% of total transactions. In 2019, AusPayNet launched the CNP Fraud Mitigation Framework to address and control this type of fraud.

Usually CNP fraud involves breaches by third parties, through hacking of IT systems of a retailer or other company. Stolen card details can then be stored by criminals and used well after the breach. Card on file transactions – where a customer keeps their card on file with a merchant they use regularly – are also becoming a preferred target of cybercriminals.

The good news about card fraud

Global fraud losses for card issuers, merchants and acquirers of card transactions from merchants and ATMs are large, totalling almost US$28 billion in 2018 – a huge increase from the US$7.6 billion lost back in 2010.[1]

Having said this though, in the past couple of years, the number of cases of payment fraud globally has been declining. This success has come through coordinated action within the payments industry, through measures including:

- a widespread roll out of chip and PIN (or chip and signature in the US) for card transactions at a physical point of sale (POS)

- the use of strong two-factor authentication for ‘card not present’ payments, as mandated in several countries

- improvements in fraud mitigation software, including the application of machine learning and artificial intelligence, and

- the roll out of tokenisation to protect card information held on file in databases and in mobile handsets.

The future of scams

Globally, the COVID-19 pandemic has seen a spike in scams seeking to exploit fears about the virus, which include targeting government payments and superannuation withdrawals. In Australia, just before the pandemic broke out in early 2020, there was also a spike in scam activity related to bushfire donations.

In response, governments and financial institutions are taking responsibility to educate themselves, consumers and businesses about the types of scams out there to help others avoid being exploited. They’re also doing more to identify and track account takeovers, shutting down “fake named” and “mule” accounts that scammers use to receive payments.

Predictions on fraud and scams are almost impossible to make, as criminals are always changing their methods and targets, partly to circumvent government efforts to address fraudulent activity. However, by having an action plan of “education, awareness and tracking”, governments, banks, consumers and businesses can take control to prevent themselves from being another scam statistic.

Looking ahead

As the world of payments continues to make strides forward, Australian consumers are likely to be at the forefront of the next evolution. At Indue, we help businesses adapt and meet the changing expectations of consumers, by delivering innovative, compliant and secure payment systems.

To learn more about the trends shaping the payments landscape and what it means for your business, contact us today

[1] Nilson Report, The Nilson Report Issue 1164, November 2019.

Orion Financial Crimes – Case Study

Fighting financial crime with award-winning technology

Orion Financial Crimes – Case Study

The growing sophistication of financial crime remains an ever-present threat, particularly as we move to a predominantly cashless society, and engage with more ways to pay. Left exposed or unprotected, fraudsters can swiftly take their toll on financial institutions’ bottom line and reputations.

To stay on top of innovative financial crime perpetrators, financial institutions must have the best people, processes and technology in place to efficiently detect and monitor fraudulent behaviour. This valuable mix can sometimes take years to develop without the support of specialist providers.

Financial institutions are often faced with having to run multiple, costly technology solutions that tackle independent payment channels. This can lead to siloed people and processes supporting these multiple solutions. Managing multiple solutions also runs the risk of delaying the detection of fraud and potentially missing a fraud event entirely, exposing vulnerabilities for fraudsters to exploit.

These were just some of the challenges Indue’s client — a well-known Australian bank — faced while attempting to protect its 400,000-plus customer base prior to engaging Indue’s financial crimes experts.

Results we achieved for a leading Australian bank

-

50% cut in fraud losses in the first month

-

60% reduction in false-positive fraud results

-

400,000-plus customers better protected

Challenges

As a leading Australian bank, reliable fraud monitoring was essential to keep up with the fast, real-time transaction speeds of today’s payments networks. The bank was fighting fraudsters without the ability to decline in-flight transactions in real time, the outcome was fraudsters had the opportunity to achieve far greater attacks utilizing velocity and speed to their advantage.

The bank’s incumbent technology was also returning significant false-positive fraud results, thereby clouding analyst assessments and creating cost inefficiencies for operations. This enabled real fraud to hide behind genuine behaviour, which was often missed during assessments.

Critically, fraud was being monitored only during office hours by the client’s operations team. This often resulted in a backlog of events for next day review, while providing an opportunity for perpetrators to schedule attacks during out of hours and unmonitored periods.

How Indue helped: 5 key priorities

Shared vision: Indue’s financial crimes experts were able to see the bigger picture and work in partnership with the bank on their longer-term business planning goals and objectives, to provide a solution that could grow and adapt over time.

Partnership: The client was seeking a supplier who would take a true partnership approach. A partner who could work with them to co-create an integrated solution that could simplify the management of multiple payment channels and return better results than its existing provider.

Partnership: The client was seeking a supplier who would take a true partnership approach. A partner who could work with them to co-create an integrated solution that could simplify the management of multiple payment channels and return better results than its existing provider.

Collaboration: A key success factor was the focus on collaboration between the client and Indue. The teams worked closely to ensure each other’s strengths were being leveraged, that the client was listened to and understood, that there was clarity on the problems that needed solving, and that there was alignment on identifying technical challenges and key performance outcomes.

Understanding: Built on years of experience, the Indue team understands that the closer you can work with a client’s team, the better the outcome. It was through establishing a close working relationship Indue was able to provide direction & guidance to help them decide how they wanted and needed to interact with the service. As the client was reshaping their own fraud management approach, Indue was able to provide guidance and counsel.

Feature Rich Service: The bank required a 24×7 alert triage service thereby providing round the clock monitoring and protection for their 400k+ customer base. Powered by award-winning IBM Safer Payments, the Indue solution was able to reduce the risks associated with the client’s multiple payment channels. Further, Indue’s investigation Case Management tool made an outsourced service much easier to manage back in the clients own shop. Finally, the Indue aggregation model was able to deliver insights from across a broad range of industry financial crime learnings, providing the client with greater visibility of the financial crime landscape.

“Financial crime is a unique, fast-paced and often highly complicated problem to solve. It requires people, process and technology working together harmoniously to achieve results.”

Dean Wyatt, Head of Financial Crimes, Indue

Results, return, future plans

Following the implementation of Orion Financial Crimes Solution, the bank saw immediate results with card fraud losses cut by 50% in the first month alone. More fraud was detected through less alerts and false-positives reduced by 60%.

Better outcomes overall were achieved in prevention and detection by addressing both fraud and scams, and significantly reducing chargebacks to customers.

The bank is now looking to add further payment channels to Indue’s solution, taking full advantage of the single-view capability of Orion Financial Crimes and IBM Safer Payments.

Critically, the bank can now focus its attention on higher value programs to drive its customer-first value proposition while working with Indue to protect its customers.

Orion Financial Crimes

Orion Financial Crime’s ability to inherently integrate people, processes and technology provides a cutting-edge solution with real-time capability, integrating artificial intelligence and machine learning to deliver a 24/7 fraud monitoring solution.

Launched in 2003, Orion Financial Crimes went live with IBM Safer Payments in 2018, providing real-time fraud & scam detection and management, anti-money laundering and counter-terrorism financing monitoring, sanctions checking across Australia and New Zealand.

Launched in 2003, Orion Financial Crimes went live with IBM Safer Payments in 2018, providing real-time fraud & scam detection and management, anti-money laundering and counter-terrorism financing monitoring, sanctions checking across Australia and New Zealand.

To find out how you can tap in to Indue’s team of experts & specialists in fraud management contact us today.

Top three 2020 financial crime trends

Top three 2020 financial crime trends

The global pandemic and subsequent economic downturn has presented a new set of challenges for financial institutions

The global pandemic and subsequent economic downturn has presented a new set of challenges for financial institutions as they work to keep pace with financial crimes across the sector. With advancements in technology, changes in human behaviour and an increase in vulnerability as a result of COVID-19, it has never been more important for organisations to remain ahead of the financial crime curve and put up a solid defence in a post-pandemic world.

As the nation continues to navigate the ‘new normal’, we took a look at the top three financial crime trends of 2020 with Indue’s Financial Crimes team as a friendly reminder to stay vigilant and safeguard against professional perpetrators.

1. Rise of ecommerce

There’s no doubt the way we choose to pay has materially changed since the onset of COVID-19. With lockdown restrictions across the country, we’ve seen traditional brick and mortar stores exchanged for convenient and contactless ecommerce channels.

As a result, ATM withdrawals and cash-out transactions have dropped considerably, with the RBA reporting a 52% and 30% decrease respectively for the quarter ending June 2020.

Meanwhile, a recent report by Australia Post revealed ecommerce has grown by a mammoth 80% year on year in the eight weeks since COVID-19 was declared by the World Health Organisation, with an average of 2.5 million households buying something online each week in April 2020, compared to 1.6 million in 2019.

This significant shift to online transactions has seen a corresponding increase in online fraud. Indue’s Head of Financial Crimes, Dean Wyatt, said the company’s internal fraud metrics in relation to ecommerce had reported a 28% rise to 98% since the global pandemic hit.

“With an increase in online traffic comes an increase in fraud associated with ecommerce merchants, putting customers’ personal details at risk,” he said.

“On the other hand, we’ve seen instances of petty theft and stolen cards decline as a result of restrictions such as curfews and people generally travelling less, including people shifting to working from home arrangements.

“The good news is we’ve been able to hone in on this change using our multi-channel Orion Financial Crimes service, and align our analytics to identify and track suspicious behaviour in real time, to ensure our customers remain protected.

“Customers need to be aware that if they’re using new types of payments, they need to be following the same rigor as you would when paying instore.”

2. The art of social engineering

Social engineering by definition seeks to exploit human psychology to access and obtain personal information, and it’s this type of scam that continues to outsmart targets.

From phishing attacks (fraudulent emails or texts that appear to come from a reputable source) to baiting (a false promise to pique a victim’s greed or curiosity), the goal of the ‘social engineer’ is to trick individuals into giving up sensitive information or visiting malicious URLs to compromise their systems.

“We have seen a strong shift to perpetrators compromising people directly and involving them in the scam, rather than solely relying on targeting accounts or cards,” Dean said.

“Compromising identity details across driver licences, passports, and email or social media accounts is hot property at the moment because financial services are inherently integrated with those types of documents, information and platforms.

“People are fooled by sophisticated attacks that purport to ‘know you’, calling with pieces of information already collected, with the intention of gathering further details from the victim. When scammers are able to access detailed personal information, they can easily create new accounts or lines of credit under individuals’ names.

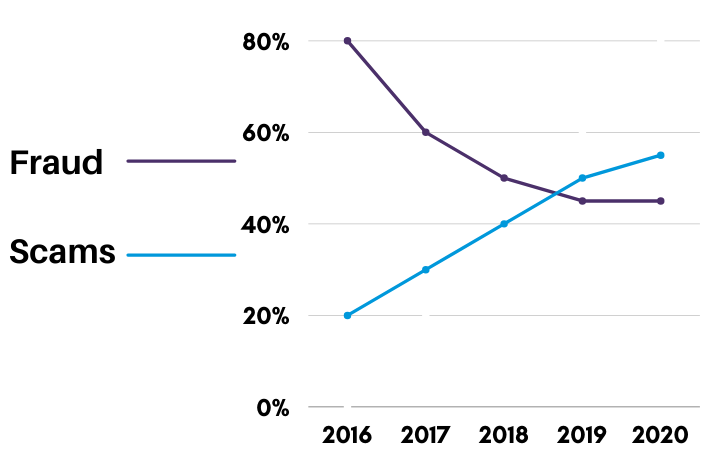

“At Indue, we have seen a considerable rise in social engineering over the last four years, to the point where it is now a larger problem than fraud. In 2016, financial crimes represented 80% fraud compared to only 20% social engineering scams, but as of 2020, we’re now seeing 45% fraud compared to 55% scams.”

“At Indue, we have seen a considerable rise in social engineering over the last four years, to the point where it is now a larger problem than fraud. In 2016, financial crimes represented 80% fraud compared to only 20% social engineering scams, but as of 2020, we’re now seeing 45% fraud compared to 55% scams.”

According to the Australian Payments Network, the most common contact method for scam activity in Australia is by email, but scams via phone result in the most financial loss.

3. Money laundering and terrorism financing

A key focus for institutions and regulators has been the growing trend of traditional financial crimes, like money laundering and terrorism financing, with both AUSTRAC and the Financial Action Task Force (FATF) reviewing controls and payment systems to identify potential weaknesses that could be exploited by criminals across the sector.

Money laundering seeks to disguise the proceeds of crime as legal income, while terrorism financing, as the name suggests, funds terrorist activities, both of which have the potential to trigger global repercussions.

Tough financial penalties have been handed down in recent times — the Commonwealth Bank of Australia and Westpac have both been hit with fines totalling $2 billion relating to serious breaches of anti-money laundering and counter-terrorism financing laws.

“With the shift of payments to a digitized world, more criminals are taking advantage of the opportunity to leverage these methods and innovative ways of sending financial transactions to each other,” Dean said.

“The rise of financial crime and the importance of protecting payment ecosystems has never been more important. With AUSTRAC’s presence increasingly felt in Australia over the last few years, I see it remaining a consistent focus beyond 2020.

“Genuine customer behaviour is certainly playing into it as well — with a strong shift to online payments, criminals are increasingly moving from hard cash to online transfer methods and attempting to hide between the genuine customer activity.

“As part of our Orion Financial Crimes solution, our anti-money laundering and counter terrorist financing service monitors customer account behaviour and transactions for unusual patterns, to detect activity that may be reportable under the Australian Anti-Money Laundering and Counter Terrorist Financing Act.”

Find out more

Learn more about Indue’s Orion Financial Crimes service, a multi-channel detection system that harnesses transactional data, customer behaviour and biometrics to expose anomalies and identify fraudulent activity. Delivered by an expert team, the service is forward-thinking with a machine learning/artificial intelligence component and places customers ahead of the curve, providing a safety net when it comes to material risks and losses.

customer behaviour and biometrics to expose anomalies and identify fraudulent activity. Delivered by an expert team, the service is forward-thinking with a machine learning/artificial intelligence component and places customers ahead of the curve, providing a safety net when it comes to material risks and losses.

References

1. https://www.rba.gov.au/payments-and-infrastructure/resources/payments-data.html

2. https://auspost.com.au/content/dam/auspost_corp/media/documents/2020-ecommerce-industry-report.pdf

3. https://www.auspaynet.com.au/sites/default/files/2020-08/Fraud_Report_2020.pdf

InFocus Cyber Security Interview

Is there a risk that security is compromised when providers compete on convenience?

Cyber security interview with Dave Hemingway by Lance Blockley, InFocus

Emerging Payments Association’s InFocus takes a look at Cyber Security, a theme that is more important than ever, following the wide-scale shift to remote working, and the increase in usage of e-commerce and digital identity.

Emerging Payments Association’s InFocus takes a look at Cyber Security, a theme that is more important than ever, following the wide-scale shift to remote working, and the increase in usage of e-commerce and digital identity.

In this first interview for InFocus, Lance Blockley is talking to Mani Amini CEO at Secure Forte and Dave Hemingway CCO at Indue.

Tokenisation – What is it and can it beat payment fraud?

Tokenisation – What is it and can it beat payment fraud?

Tokenisation seems to be one of the key buzzwords in the payment industry at the moment. However, what does this concept really mean and how does it benefit payments made today?

What is Tokenisation?

Tokenisation is a method of protecting sensitive data by replacing it with an algorithmically-generated number referred to as a ‘token’. In the payments world, tokenisation is commonly used to replace debit and credit card numbers in an attempt to prevent card fraud.

Under this form of tokenisation, a cardholder’s Primary Account Number (PAN) is replaced by a random number that is not linked to the card number prior to processing a transaction through the payments network. This process assists in mitigating the risk of exposing sensitive card data to unauthorised individuals or software that could potentially exploit the data by fraudulently duplicating the card details. It also prevents merchants from storing the PAN in databases, which are targets for hackers. Tokens cannot be decrypted or reverse-engineered. The only relationship between the original card number and its associated token number resides within the Token Service Provider.

What is a Token Service Provider?

A Token Service Provider (TSP) is a service provider that issues tokens, manages the lifecycle of tokens and stores the payment credentials associated with the tokens. TSPs can be an independent third party from the payment network or can be the actual card scheme (i.e. Visa, MasterCard, eftpos). TSPs must conform to strict security and privacy specifications defined by the global payment schemes and fall within the PCI-DSS compliance requirements.

Tokenisation in the Industry

Tokenisation takes many forms within the payments industry. One of the most prevalent uses of tokenisation is within the Mobile Payments space. When a cardholder provisions their payment card within an Apple or Google mobile wallet, the request is sent to the appropriate TSP to tokenise the card number. The token is then sent back to the mobile wallet for activation. The cardholder’s actual card number is never stored on the mobile device and as such cannot be extracted for misuse. All subsequent mobile transactions will use the token number as the payment credentials.

Tokenisation for in-app purchases is also on the rise due to its convenience. Some in-app purchases leverage the mobile payment functionality whereby the token stored on the mobile wallet is used to make a purchase within the phone application. An example of this would include purchasing tickets on the Ticketek app and instead of inputting credit card details, the user is able to select the Apple Pay option, which references the credentials stored within the mobile wallet. Not only does this option provide an easy streamlined purchase journey, it also removes any sensitive data from the transaction.

Tokenisation for in-app purchases is also on the rise due to its convenience. Some in-app purchases leverage the mobile payment functionality whereby the token stored on the mobile wallet is used to make a purchase within the phone application. An example of this would include purchasing tickets on the Ticketek app and instead of inputting credit card details, the user is able to select the Apple Pay option, which references the credentials stored within the mobile wallet. Not only does this option provide an easy streamlined purchase journey, it also removes any sensitive data from the transaction.

Tokenisation for card-on-file online purchases is also becoming more common given the recent occurrences of global data breaches. Wawa, a popular convenience store chain in the United States, confirmed in late 2019 the discovery of malware on their payment processing servers. The malware captured credit and debit card numbers, cardholder names and expiration dates. Card-on-file tokenisation protects a cardholder’s card credentials stored at online merchants with whom the cardholder frequently make purchases. Netflix holds the card credentials of all its customers for the purpose of charging the monthly subscription fees. The streaming service provider has recently undertaken a significant exercise of tokenising as much of its database as possible as a means to mitigate the risk of data breaches. As more online merchants migrate to tokenisation, the prevalence of card data breaches will hopefully decrease as well. Given that a new unique token is generated for each retailer, a security breach at one retailer will not compromise the security of the token data at another retailer.

Payment Account Reference – Providing a holistic view

Although the use of tokenisation enhances the security of digital payments, it also presents a challenge. If a cardholder’s card credentials are tokenised for use within Google Pay on an android phone, Apple Pay for an iPad and Netflix for monthly subscription payments, it becomes a one to many relationship. One single PAN is now linked to several tokens across different systems and platforms.

As only the TSP has the original data linking the PAN to the multiple tokens, the lack of visibility makes it difficult for other parties such as merchants to have a consolidated view of all transactions performed by the cardholder and subsequently provide value-add and compliance services. An example of this is the provision of fraud and anti-money laundering monitoring services. To provide the most effective service, there is a need to identify transactions on an aggregate card level to better assess customer behaviour and payment trends.

As a means to provide a consolidated view, some card schemes have introduced the use of a Payment Account Reference (PAR). According to a recent white paper published by EMVCo, a global entity facilitating worldwide interoperability of secure payment transactions, a PAR is a ‘non-financial reference assigned to each unique PAN and used to link a Payment Account represented by that PAN to affiliated Payment Tokens’. PAR is passed in the transaction message to the merchant so that they can reference this field when performing customer level analysis.

EMVCo affirms that this is a long term solution that will solve the issue by linking together disparate card-based and token-based transactions without compromising on security. Although this is the recommendation of EMVCo, it is the responsibility of the card payment schemes to adopt this concept and implement it into their respective payment ecosystems. eftpos is introducing support for PAR in the near future.

Resources:

Card-Not-Present (CNP) Fraud Mitigation Framework

Card-Not-Present (CNP) Fraud Mitigation Framework

The banking industry has commenced the execution phase of this framework, which aims to tackle the most prevalent type of card fraud.

Long gone are the days when a cardholder could only make a purchase at point of sale with their physical card. The ongoing advances in payment capability previously paved the way for consumers to make online Card-Not-Present (CNP) transactions, but has now gone even further by enabling these CNP transactions to be initiated from a mobile wallet with fingerprint authentication.

Nevertheless, the fundamental transaction that underpins these digital advances is the CNP transaction, which is gaining momentum as one of the most popular ways Australians like to transact. The CNP transaction growth rate has increased from 14% in 2017 to 27% in 2018*, which may be partially accounted for with the increase of mobile in-app payment opportunities (where a consumer uses a retail app and selects a card stored in their mobile wallet to make the purchase). More avenues for CNP transactions means more opportunities for card compromise and fraud spending.[/vc_column_text][vc_column_text el_class=”ind-textBox”]

CNP Fraud Mitigation Framework

Earlier in the year, Indue advised its clients of the significant industry-wide initiative to combat the increasing CNP transaction fraud. Championed and led by the Australian Payments Network (AusPayNet), the CNP Fraud Mitigation Framework aims to target the most prevalent form of fraud in the card payments space.

According to AusPayNet’s ‘Australian Payment Card Fraud 2019’ report, although the rate of CNP fraud growth has decreased since previous years, CNP fraud still accounts for 85% of all card fraud on Australian cards.

The collective industry acknowledged the need to address this fraud concern by establishing this industry-wide framework.

CNP Mitigation Framework in Action

The CNP Mitigation Framework took effect in 1 July 2019 after a long collaboration and consultation process to define the minimum standards that both card Issuers and Merchants need to meet as a means to reduce the rates of CNP fraud. These standards provided industry-agreed fraud thresholds that Issuers and Merchants were to report against. Failing to meet these thresholds would require them to implement additional security measures or be subjected to penalties. “Breaches of these thresholds will trigger obligations for Merchants and Issuers to take action. Repeated breaches over a period of time could ultimately result in financial penalties for Issuers or Merchants’ Acquirers,” AusPayNet said in an industry release.

Watch and See

In July 2019, Indue consolidated the required statistical data on behalf of our financial crimes clients and submitted the relevant reporting to AusPayNet. Indue has since continued to submit monthly reporting to AusPayNet according to the CNP Fraud Mitigation Framework requirements. As this new reporting becomes embedded in the operation and maintenance of the card payments ecosystem, AusPayNet and indeed the entire industry will get a glimpse into whether this new framework is making inroads into the chief objective of curtailing the growth of CNP fraud. Coupled with the 3DS 2.0 mandate issued by both Visa and MasterCard, this reporting and accountability should have an impact on fraud numbers. It will be an interesting space to watch over the next two to four years.

References

*Source: Reserve Bank of Australia

AusPayNet’s Australian Payment Card Fraud 2019 report

Indue’s March 2019 CNP Fraud Mitigation Framework article

Card Not Present (CNP) Fraud: Keeping Pace in the Fraud Race

Keeping Pace in the CNP Fraud Race

The Australian payment industry has seen a seismic shift in the past few years from traditional retail store purchases to online shopping. This migration coupled with the strong fraud protection provided by EMV chip technology for in-person transactions has unfortunately prompted an adverse mirrored trend – an increase of fraud in card not present channels. Card not present (CNP) fraud now accounts for almost 85% of all card payment fraud in Australia and further to this, CNP fraud seems to be growing 13% year on year at an industry level.

To combat this increased threat, AusPayNet in conjunction with key industry stakeholders have initiated an industry-wide collaboration program entitled the ‘Card Not Present Fraud Mitigation Framework’. This Framework sets out the industry approach to mitigate CNP payments fraud for all members across the payment value chain – merchants, consumers, Issuers, Acquirers, card schemes, payment gateways, payment system providers, and regulators. It is a framework designed to reduce fraud in CNP online channels, while also ensuring that online transactions continue to grow and thrive. The key tenets of this framework have been established by the industry:

Guiding Principles

1. Consistently apply Strong Customer Authentication (defined below)

2. Leverage global standards and best practice from other jurisdictions where possible

3. Be technology neutral to provide choice and ease of implementation

4. Use dynamic data wherever possible to reduce fraud

5. Act now, plan for the future – deal with the current fraud issues with the ability to review and update the Framework over time.

Card Not Present (CNP) Fraud Framework: Issuer Obligations

This framework requires participants across the payment value chain to take a more active role in reducing Card Not Present (CNP) fraud. For Card Issuers in particular, the two main obligations within this new framework are as follows:

• Ensure fraud rate remains below Issuer Fraud Threshold

• Perform Strong Customer Authentication or Risk Based Authentication when requested by the Merchant

This framework has set an industry fraud benchmark for an acceptable level of Issuer and merchant risk. Quarterly reporting to AusPayNet of fraud rates will be mandated as part of this framework. Issuers and merchants with fraud rates under the established threshold will not be required to perform any additional fraud mitigation activities. Issuers and merchants operating over the industry fraud rate will be required to perform Strong Customer Authentication. Should Issuers and merchants continue to breach industry thresholds over consecutive quarters, fines and sanctions can be imposed.

Strong Customer Authentication (SCA)

SCA is an authentication method requiring the cardholder’s identity to be verified with at least two independent factors from the following categories:

1. Something only the cardholder knows (knowledge factor) – a password, an answer to a secret question or a PIN

2. Something only the cardholder possesses (possession factor) – a credit card, a hardware token or a smartphone

3. Something the cardholder is (inherence factor) – a biometric feature such as a fingerprint scan, an iris scan, or facial recognition; or a behavioural feature such as type or swipe dynamics.

Although cardholder authentication will actively reduce the occurrence of fraudulent activity, the industry must also consider the user experience when implementing an authentication solution. The framework should provide the consumer with confidence that online transactions are secure without adding a disproportionate degree of friction to the transaction journey.

Card Not Present (CNP) Fraud Framework: Implementation Timeline

The industry timeline for the implementation of the framework is outlined below: fraud implementation timeline")

Indue has been involved with developing the industry-wide framework via representation and collaboration at forums and consultation submissions. Indue has commenced an internal program of work to build the capability to support the required AusPayNet reporting. We will work closely with all of our card issuers in the next few months to ensure understanding of the initiative requirements and next steps to comply with the new framework.

Update

The banking industry has commenced the execution phase of this framework, which aims to tackle the most prevalent type of card fraud Read our follow up article here.

Indue Reinvents its Financial Crimes Service

Indue Reinvents its Financial Crimes Service in the Australian Mutual Sector

An IBM Client Story

The New Payments Platform (NPP) opened up an opportunity for Indue to reinvent our financial crimes service in the mutual sector due to the potential increased risk with NPP over traditional channels.

The New Payments Platform (NPP) opened up an opportunity for Indue to reinvent our financial crimes service in the mutual sector due to the potential increased risk with NPP over traditional channels.

Dave Hemingway, our Chief Product Officer, discussed how Indue’s relationship with IBMs safer payment solution has resulted in the following benefits:

- Lower false positive rates by 20% improvement.

- ability to make rule changes 90% faster.

- manage all payment channels in one system.

{kind=link}